So, you’ve found a house that could be great if only it had a new roof, updated kitchen, or finished basement. You’re thinking about using an FHA 203(k) loan to make it happen, but first, you need to answer the big question: Is this even feasible? Let’s walk through exactly how we approach a quick 203(k) feasibility study so you know what to expect and how it helps you as a buyer or homeowner.

What Is a 203(k) Feasibility Study?

A 203(k) feasibility study is a detailed first look at the condition of the property and what it would take to bring it up to FHA’s minimum standards, plus any upgrades you might want to add.

We assess:

- Whether the property qualifies for a 203(k) loan.

- What mandatory repairs are required to meet the FHA minimum property standards.

- What upgrades or renovations would you like to include.

- The rough cost of everything.

- If the total project fits within FHA loan limits and your personal budget.

It’s a big-picture analysis that helps you make informed decisions before moving forward with formal estimates or loan paperwork.

What’s Included in a Feasibility Study?

When we do a 203(k) feasibility study, we include all the key elements needed to make a smart decision:

- General condition of the property

We check for signs of deterioration, water damage, outdated systems, structural issues, and more. - FHA minimum property standard compliance

We specifically look at what the FHA requires for a home to be considered safe and livable. This includes things like:- Working plumbing and electrical

- A sound roof with no leaks

- Safe stairs and handrails

- No broken windows or damaged doors

- No mold, asbestos, or lead-based paint issues (especially in homes built before 1978)

- List of required vs. desired improvements

Required repairs are things the house must have to qualify for FHA financing. Desired upgrades are things you want to improve while you’re renovating like updating a kitchen or finishing a basement. - Rough cost estimates

We provide a rough cost estimate so you can see what you’re working with. - Estimated project timeline

Limited 203(k) projects must be completed within 9 months, and standard 203(k) projects must be completed within 12 months after closing. We’ll assess whether that’s realistic for your scope. - After-repair value (ARV)

We help you understand what the home could be worth once all the work is complete.

When Is a 203(k) Feasibility Study Required?

Technically, an official 203(k) feasibility study provided by a HUD-approved consultant is only required for standard 203(k) loans, especially when you’re doing major renovations or structural changes.

But honestly? Even if you’re using a limited 203(k), it’s still super helpful to do a quick feasibility study. It can prevent surprises and save you from losing money.

Here’s when it’s most useful:

- You’re not sure if the repairs fit within the $75k cap of a Limited 203(k).

- The house needs work, but you’re unsure how deep the problems go.

- You’re deciding between multiple fixer-uppers and want to compare.

- You want to negotiate a better deal based on needed repairs.

Whether you’re a buyer, a homeowner refinancing with a 203(k) loan, or an investor looking to live in one of the units, this first step saves time and money later.

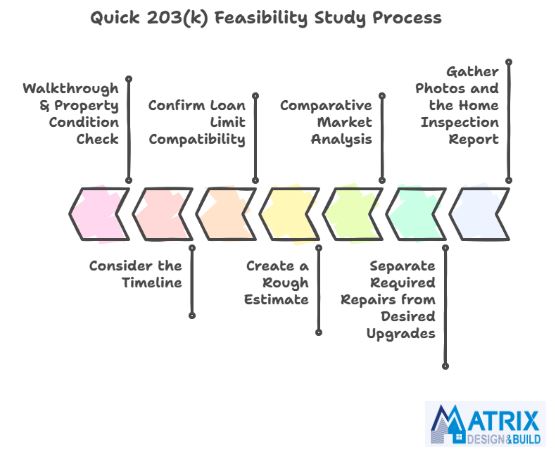

7 Steps to Do a Quick 203(k) Feasibility Study

Here’s a detailed look at how we, as your contractor, walk through a quick 203(k) feasibility study. This is how we get you the information you need fast.

1. Gather Photos and the Home Inspection Report

We start by sending you a simple photo guide that walks you through how to take and share the right pictures of the property. These photos help us understand the home’s current condition, what looks solid, and what might need attention. If you already have a home inspection report, this is the time to share it with us, too. It gives us a head start in identifying any major issues and allows us to focus on what matters most during the feasibility review.

We look for:

- Roof condition (leaks, age, sagging)

- Foundation cracks or water intrusion

- Damaged or outdated electrical wiring

- Broken or missing handrails

- Plumbing leaks or missing fixtures

- Old HVAC systems

- Water damage, mold, or signs of pests

- Windows and doors that don’t open, close, or lock properly and much more.

If any of these things are present, they’ll be part of the required repairs list.

2. Separate Required Repairs from Desired Upgrades

Next, we help you split the renovation list into two categories:

- Required Repairs: These are things that must be fixed for the home to be brought up to FHA standards. Without fixing these, the home won’t qualify for a 203(k) loan.

- Desired Improvements: These are the upgrades you want for your own comfort or to boost the value, like installing new kitchen cabinets, adding a deck, or modernizing a bathroom.

Having this breakdown helps keep your renovation goals realistic while still giving you space to dream a little.

3. Comparative Market Analysis

Based on the information we’ve gathered, we create a Comparative Market Analysis (CMA) report. So, what exactly is a CMA? A Comparative Market Analysis (CMA) is a report prepared to estimate a property’s current market value. It’s based on the prices of recently sold, active, and pending homes that are similar in size, condition, location, and features.

A CMA helps you figure out what a property is worth in today’s market before you make an offer or plan any renovations.

4. Create a Rough Estimate

Next, we prepare a rough scope of work along with a preliminary cost estimate. This gives you a general idea of what the project might involve and helps you decide whether to move forward. While this isn’t a detailed line-by-line estimate, we focus on giving you the most realistic rough number possible. So you have a solid starting point for decision-making.

5. Confirm Loan Limit Compatibility

We’ll help you add up the purchase price + renovation costs + contingency + fees (permits, inspections, consultant fees, etc.) and make sure the total stays under the FHA loan limit for your county.

If you’re getting close to that limit, we might revise the scope or look for other cost-saving options.

6. Consider the Timeline

Finally, we evaluate whether the job can realistically be completed within the 9 or 12 months deadline set by FHA. If it’s a bigger renovation, we’ll talk through how to schedule phases of the work and what might be needed to stay on track: permits, inspections, material orders, etc.

At this stage, we can determine whether the project is financially feasible. If it’s not, we’ll work with you to adjust the scope of work and explore alternative options to make it more viable.

If it is feasible, great news! You’re now in a position to confidently make an offer on the property.

7. Walkthrough & Property Condition Check

Once your offer is accepted, we schedule a detailed walkthrough of the property. During this visit, we carefully inspect each area and take notes on everything that needs to be addressed. From there, we create a comprehensive scope of work, outlining each item with clear, simple descriptions. For example:

- Replace the existing roof

- Install new HVAC and ductwork

- Update the electrical panel and rewire the house

- Full kitchen remodel with cabinets and countertop

- Refinish basement (600 sqft)

- Repair rear deck stairs and railing

Then, we attach numbers to each item based on our experience and current market prices.

How Long Does It Take?

We can usually complete a quick 203(k) feasibility study within 3 to 5 business days after we get all the information we need from you. It’s fast, but it gives you a solid foundation to make your next move.

What Happens After the Report Is Done?

If everything looks good, your budget works, the loan limit isn’t maxed out, and the ARV supports the value, then we move to the next steps:

- You apply for the loan with your lender.

- A 203(k) consultant (if required) performs the official study and Work Write-Up.

- We provide a formal contractor estimate to match that Work Write-Up.

- You close on the loan.

- We schedule permits, order materials, and start construction.

The Benefits of a 203(k) Feasibility Study

Doing this step first saves time, money, and stress down the line. Here’s why:

For Homebuyers

If you’re buying a fixer-upper with a 203(k) loan, the feasibility study helps you figure out if the deal makes sense. It outlines the exact repairs needed to bring the home up to FHA’s minimum standards and gives you a rough renovation budget before you even make an offer.

That’s huge. Because without knowing what the repair costs look like upfront, you could be offering more than the home is worth after it’s fixed.

Plus, once you have this report in hand, you can:

- Adjust your offer based on actual repair needs

- Use the findings to negotiate a better price

- Quickly decide whether to move forward or walk away

For Sellers

Selling a property that needs work? A 203(k) feasibility report can help you price it smarter and sell it faster.

By having the report ready before you list, you show buyers, especially those using 203(k) loans, what the property needs and how much the repairs will cost. That builds trust and can make your property stand out compared to others that come with too many unknowns.

And here’s the kicker: The FHA 203(k) loan allows buyers to borrow up to 110% of the after-repair value (ARV). That means your home could sell for more than its current “as-is” value if the future potential is clear and documented.

This is especially helpful if your home is likely to attract first-time buyers using FHA financing.

For Real Estate Agents

As an agent working with buyers or sellers on rehab properties, a 203(k) feasibility study gives you a huge edge.

You’ll have a professionally written, detailed report that outlines:

- What the property needs

- What will it cost

- Whether the numbers make sense

This helps your buyer clients feel confident making offers and helps your sellers back up their asking price.

You can also team up with 203(k) loan lenders, contractors and consultants to create a smooth, all-in-one buying experience.

For Contractors

For contractors, a 203(k) feasibility study is a great way to build trust early in the process by showing clients you understand the scope, budget, and FHA requirements from day one. It helps you identify potential issues before they become expensive problems and allows you to plan materials, labor, and timelines more accurately, minimizing surprises and making the entire project run smoother.

Conclusion

A 203(k) feasibility study doesn’t have to be complicated, and you don’t need to wait weeks for answers. As your contractor, we can walk through the house with you, spot the repairs that matter, estimate the work, and give you a clear roadmap forward.

It’s not just about fixing a house, it’s about building a future you feel good about.

Let us know when you’re ready. Then we’ll handle the heavy lifting so you can focus on what’s next. Contact us for a FREE Consultation!

0 Comments