Buying a home can be an exciting journey, but it often comes with its fair share of challenges. One of the most common hurdles? Appraisal issues. Low appraisals can derail the purchase of your dream home, especially if you’re planning to renovate. Luckily, there’s a solution: overcoming appraisal issues with a 203(k) loan. This unique financing option not only resolves appraisal issues but also allows you to access 110% financing to cover purchase and renovation costs. With this powerful tool, you can transform any property into your dream home without financial roadblocks. Ready to learn more about it?

Understanding the Basics of 203(k) Loans

An FHA 203(k) loan is a government-backed mortgage that bundles the cost of purchasing a home and the expenses of renovations into a single loan. It’s designed for properties that need repairs or updates and helps buyers avoid the hassle of separate financing for renovations.

Key Features:

- Single Loan: Combines the purchase price and renovation costs.

- Low Down Payment: Typically 3.5% of the combined loan amount.

- Flexible Eligibility: Available for first-time buyers, repeat buyers, and investors under certain conditions.

- Renovation Funds: Covers structural repairs, cosmetic upgrades, and even major projects like adding a second floor.

What is an Appraisal, and Why Does it Matter?

An appraisal is an independent assessment of a property’s value, typically conducted by a licensed appraiser. It’s a critical step in the home-buying process because lenders rely on it to determine how much they’re willing to loan.

The Problem with Low Appraisals?

A low appraisal can throw a wrench in your plans. Imagine finding your perfect home, only to have the appraisal come in lower than the agreed-upon purchase price. This often means:

- Paying the difference out of pocket.

- Renegotiating the price.

- Losing the property altogether if financing falls through.

This is where the 203(k) loan and its 110% financing feature come to the rescue.

How a 203(k) Loan Solves Appraisal Problems

The 203(k) loan, backed by the Federal Housing Administration (FHA), is a game-changer. Unlike traditional loans, which base financing on the current appraised value, a 203(k) loan considers the after-repair value (ARV)—the estimated value of the home after renovations are complete.

And here is the best part:

One of the standout features of a 203(k) loan is the ability to finance up to 110% of the ARV. This means you’re not just covered for the purchase price and renovation costs but also have a cushion for unexpected expenses or ambitious upgrades.

Let’s Break It Down with a Scenario:

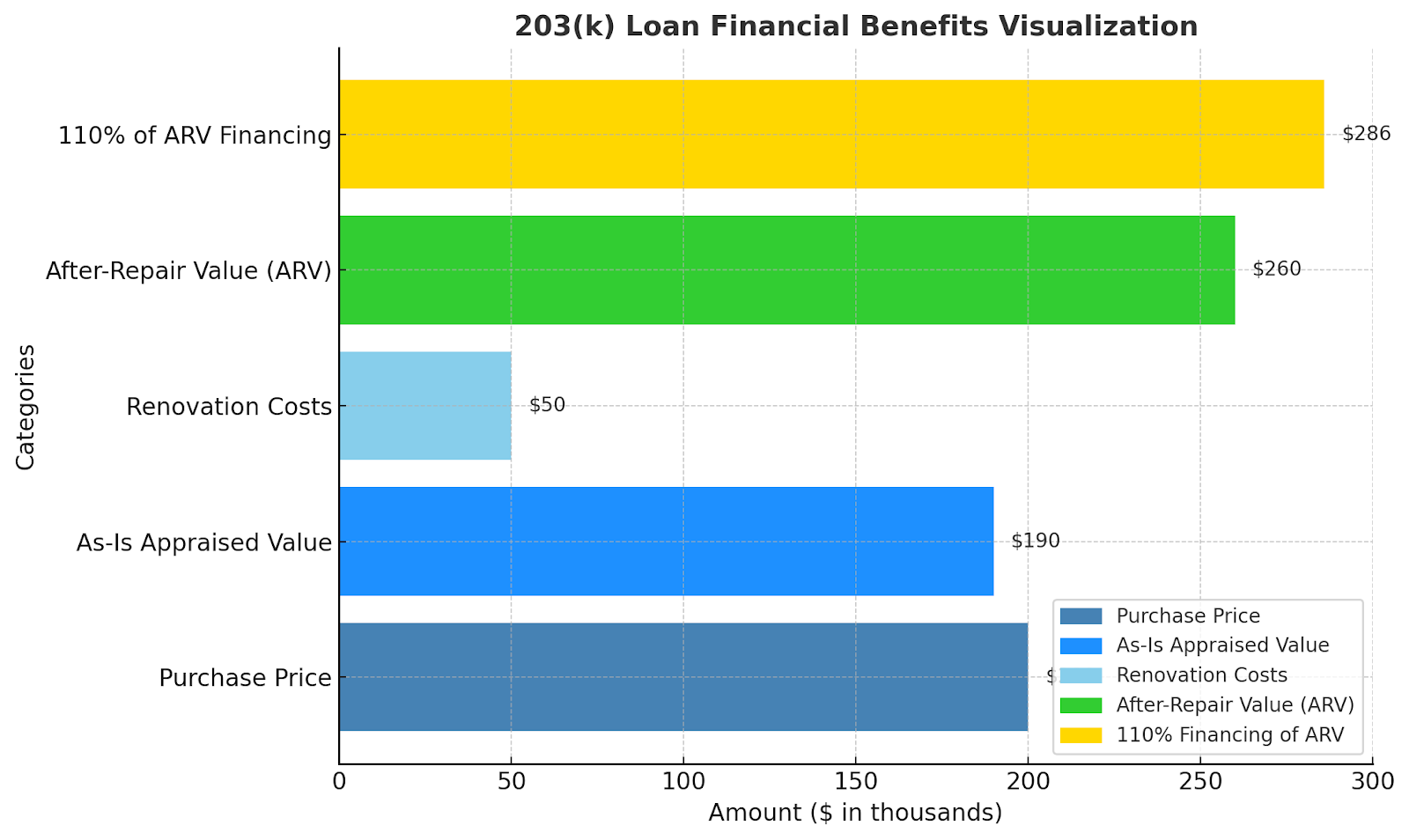

You find a home in Philadelphia listed for $200,000. It’s a great deal, but the property needs $50,000 in renovations to modernize the kitchen, update the bathrooms, and replace the roof.

- As-Is Appraised Value: $190,000 (Due to required repairs)

- After-Repair Value (ARV): $260,000

With a traditional loan, financing would only cover the $190,000 appraised value, leaving you to pay $60,000 out of pocket for the purchase and renovations.

With a 203(k) loan:

- You can secure funding based on 110% of the ARV, which is $286,000.

- This covers the $200,000 purchase price, $50,000 in renovations, and additional funds for unforeseen costs.

Now, instead of losing the deal or stretching your finances, you’re empowered to transform the property into your dream home.

Now you can see how overcoming appraisal issues with a 203(k) loan comes true!

Overcoming Appraisal Issues with a 203(k) Loan: 110% Financing

Getting 10% more than the appraised value is exciting on its own, but let’s dive into why this extra cushion is so impactful:

1. Flexibility for Renovations

The extra 10% allows you to handle surprises during the renovation process, whether it’s hidden structural issues or design upgrades you didn’t initially plan for.

2. Maximizing Borrowing Power

By accessing 110% financing, you can confidently bid on homes needing significant repairs without worrying about appraisal gaps or additional out-of-pocket expenses.

3. Dream Big with Customization

With funds for both purchase and renovations, you can transform a fixer-upper into a completely customized home tailored to your needs and style.

What Makes 203(k) Loans Different from Traditional Loans

1. Incorporating the ARV

Traditional loans only consider the current value of the property. A 203(k) loan calculates the future value after renovations, giving you more financial flexibility.

2. No Out-of-Pocket Renovation Costs

By including renovation expenses in your mortgage, a 203(k) loan eliminates the need for high-interest credit or personal savings for repairs.

3. Building Equity Faster

Renovating with a 203(k) loan often increases the property’s value significantly. Buyers may immediately gain equity, providing long-term financial benefits.

Example: A buyer purchases a home for $150,000 and spends $50,000 on renovations using a 203(k) loan. Post-renovation, the property appraises at $225,000, yielding $25,000 in instant equity.

4. Access to Distressed Properties

With a 203(k) loan, you can consider homes that need repairs—properties that traditional lenders might overlook due to low appraisals.

Buyers aren’t limited to move-in-ready properties. They can consider distressed homes, foreclosures, and properties in desirable neighborhoods that require work.

This flexibility allows access to more affordable homes that can be customized to personal tastes.

Common Questions About 203(k) Loans

- Can I use a 203(k) loan for minor repairs only?

Yes! Limited 203(k) loans are perfect for minor upgrades under $75,000, making them ideal for quick fixes and cosmetic improvements.

- Do I need a high credit score to qualify?

Not necessarily. The FHA’s flexible requirements make 203(k) loans accessible to many buyers, with credit scores as low as 580 often accepted.

- What renovations are covered?

Everything from structural repairs to cosmetic updates like flooring, painting, or even adding a second story.

- Are there limits to the loan amount?

Yes, the maximum loan amount is subject to FHA loan limits for your area, but the inclusion of 110% of the ARV provides additional flexibility.

- Can I refinance my current home with a 203(k) loan?

Absolutely! If your home needs upgrades, you can refinance into a 203(k) loan to cover renovation costs.

- What happens if my renovation costs exceed the estimated budget?

That’s where the extra 10% of financing comes in handy. It provides a cushion for unforeseen expenses during the renovation process.

- Is a 203(k) loan only for single-family homes?

No. It can also be used for multi-family homes (up to four units) and certain mixed-use properties, as long as the primary use is residential.

Conclusion

In a nutshell, overcoming appraisal issues with a 203(k) loan has made easy. Whether you’re a first-time homebuyer or a seasoned investor, a 203(k) loan can make appraisal issues a thing of the past. Embrace the chance to renovate, build equity, and create a space that’s truly your own.

With a 203(k) loan, low appraisals don’t mean walking away from a deal. Instead, they become opportunities. Buyers can unlock the potential of undervalued properties, turning them into customized dream homes with the financial support of an FHA-backed loan.

Contact us today to explore your options and start turning challenges into opportunities. Your dream home is just a 203(k) loan away!

![Philadelphia Sump Pump Installation Requirements [2025 Guide]](https://matrixgc.com/wp-content/uploads/2025/06/Philadelphia-Sump-Pump-Installation-Requirements-2025-Guide.png)

0 Comments