Buying a home is a big deal. It’s the most significant investment you will ever make. So, you have to get it right! That’s where a home inspection comes in handy. It’s like a quick check-up for your future home to see if it’s a good pick. Everyone buying a home should get one done by a Home Inspector.

Let’s talk about people buying a home using a 203(k) loan. It can get a bit confusing because there’s another party involved – a HUD Consultant. People often wonder, “Do I still need a home inspection for a 203(k) loan? And what’s the difference between a Home Inspector and a HUD Consultant?”

Okay, it can be a bit confusing. So, let’s break it down, starting with the basics.

Who is a Home Inspector?

A Home Inspector is professionally trained and certified to evaluate the condition of residential properties. Their primary role is to conduct thorough inspections of homes, typically before finalizing a sale or as part of a homeowner’s routine maintenance plan.

During a home inspection, the inspector will examine the interior and exterior of the home, including its foundation, walls, roof, plumbing, electrical systems, heating and cooling systems, insulation, ventilation, and other essential features. They look for signs of damage, defects, code violations, safety hazards, and other issues that may need attention.

Ultimately, they prepare a home inspection report including any areas of concern and recommendations for repairs or further evaluation by specialists if necessary. This report helps buyers make informed decisions about purchasing a property. It provides sellers with insights into any necessary repairs or maintenance tasks that may help improve the marketability of their home.

Who is a HUD Consultant?

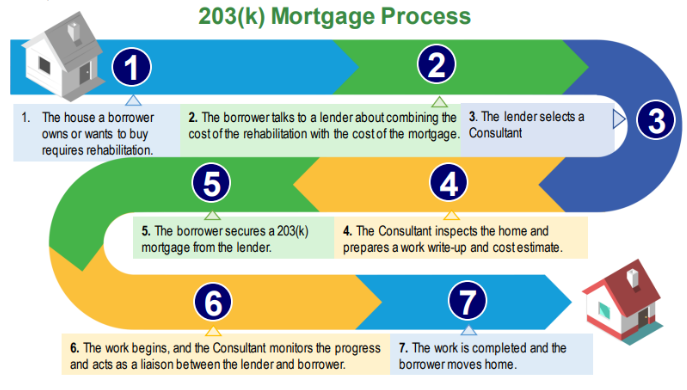

Now, let’s discuss who a HUD Consultant is! Why do you need to know this? Because for Standard 203(k) loans, the involvement of a HUD Consultant is required!

A HUD Consultant, also known as a HUD-approved 203k Consultant, is a certified professional designated by the Department of Housing and Urban Development (HUD) to oversee the renovation projects financed through the FHA 203(k) loan program.

Their primary responsibility is to assist borrowers and lenders in ensuring that the renovation projects meet FHA standards and guidelines. The consultant’s involvement spans from the initial assessment to the project’s completion.

But what exactly does their role entail during the renovation process?

- Conduct property assessments and inspections to identify the repairs needed to meet HUD’s Minimum Property Requierments (MPR) and the optional restorations you wish to make past the required projects.

- Prepare documents for the lender to figure out the loan amount and underwrite the funding, including the scope of work, cost estimates, and suggested “contingency funds” (in case there are cost overruns)

- Monitor the progress of the renovation project to ensure compliance with the agreed-upon scope of work.

- Verify the renovations’ completion and ensure that the property meets FHA standards before loan funds are disbursed.

It’s a comprehensive approach that guarantees the renovation meets both regulatory standards and the homeowner’s expectations.

IMPORTANT NOTE: For the limited 203(k) loan, the involvement of a HUD Consultant is NOT mandatory. However, consulting with a consultant at the beginning of the process is highly recommended to ensure the proposed work meets FHA minimum standards. This step can help avoid potential issues down the road.

Let’s Clarify the Difference between a Home Inspector and a HUD Consultant!

The roles of these professionals are entirely different. A HUD Consultant’s primary task is to ensure the property meets HUD’s Minimum Property Requirements (MPR) to qualify for the 203(k) loan. They also oversee the project’s progress to ensure the contractor fulfills their obligations per the contract so that the lender can disburse the funds. On the other hand, a Home Inspector’s role is to identify potential problems or issues with the property per the homeowner’s or buyer’s request. A Home Inspector provides the buyer with a snapshot of the home’s overall condition. They may reveal a significant issue that would cause a buyer to back away and terminate the contract.

It’s important to note that an inspector doesn’t “pass” or “fail” a house for an FHA loan. Instead, they provide buyers with a comprehensive overview of any issues present in the house. While the HUD Consultant can require specific fixes or repairs, their assessment may not directly align with the inspection. HUD Consultants primarily focus on safety, security, and value issues. Although the inspector may include these items in their report, they may also note other aspects not mandated by FHA.

Do I Need a Home Inspection for a 203(k) Loan?

The need for a home inspection is a common question, and the answer isn’t one-size-fits-all. It depends mainly on the scale of your project. A home inspection is highly advisable if you’re updating a kitchen, painting, and laying new floors.

Here’s why: While your contractor may quote you for the kitchen, paint, and flooring, their focus is not on inspecting the overall condition of the property. On the other hand, a Home Inspector inspects the plumbing, electrical systems, roofing, and all the home components to ensure they are in good working order.

This distinction is essential. Your contractor’s estimate only includes the specific work you want to have done.

On the other hand, if your project involves a comprehensive renovation with new roofing, electrical, plumbing, HVAC systems, and overall finishes, you might wonder if a home inspection is necessary. Well, essentially, not entirely!

Because in this situation, the contractor is already inspecting your entire house. Moreover, extensive renovation projects typically fall under the standard 203(k) loan category, which involves the involvement of a HUD Consultant responsible for inspecting the entire property. Thus, while considering a home inspection for a 203(k) loan may not be as crucial in this scenario, having an additional set of eyes can still be beneficial.

So, what’s the best course of action?

Whether you are undertaking a minor update or a major renovation, considering a home inspection for a 203(k) loan is a prudent step that can help ensure the success and integrity of your renovation project.

Conclusion

Now that you understand the roles of a Home Inspector and a HUD Consultant, let’s bring it all together.

Regarding a standard 203(k) loan, which mandates the involvement of a HUD Consultant, the necessity for a home inspection may seem less pressing. However, for a Limited 203(k) loan where a HUD Consultant is not mandatory, opting for a home inspection is a wise choice to ensure you’re making a sound investment.

Remember that the contractor plays a pivotal role in the success of any 203(k) renovation project. That’s where Matrix Construction steps in. As your trusted contractor serving Philadelphia and New Jersey, we’re here to provide you with a FREE Consultation and Estimate, addressing any concerns or questions you may have along the way.

With Matrix Construction by your side, you can confidently embark on your 203(k) renovation journey, knowing you have the support and expertise to bring your vision to life.

![Top 20 Reasons for Failing a Plumbing Inspection in Philadelphia [2025 Guide]](https://matrixgc.com/wp-content/uploads/2025/05/Common-issues-causing-failing-a-plumbing-inspection-in-Philadelphia.png)

This article delves into a crucial aspect of securing a 203(k) loan – the necessity of a home inspection. The thorough exploration of whether a home inspection is required provides valuable insight for individuals navigating the loan process. Understanding the implications of a home inspection on the 203(k) loan journey is essential for making informed decisions. Thanks for shedding light on this topic and offering clarity to prospective borrowers!

Fosroc Construction Solution

We’re glad you found the article helpful! Understanding home inspections and the 203(k) loan process is a common concern, and we’re happy to clarify.

If you have any further questions about 203(k) loans or home inspections, don’t hesitate to reach out! We’re here to help you.